W..T..F? . . .

. . . What’s up with The Funds?

This post will present documentation that will show:

· a large sum of money unaccounted for

· actions taken without formal Board approval

· official actions being taken without Board resolution (as required by PA state code)

· a suspected attempt to move money around to hide its availability

It will also show:

· FC administrators lack of respect for Board authority

· FC’s former board president overstepping his bounds and authority

· FC's lack of openness to the public that is required under the Sunshine Act

------------

FC has posted the 2010-2011 Annual Financial Report on its website. (http://www.fortcherry.org/170310111811173687/lib/170310111811173687/_files/AFR.pdf)

This report is submitted annually to the PDE through the PA Office of the Budget, Comptroller Operations.

Page 4 of the AFR depicts the balance of FC’s major funds.

As you can see, the AFR shows that FC has $1.3 million dollars tied up in a COMMITTED FUND.

FC is reporting a $1.3 million fund balance in a Committed Fund to the state . . .

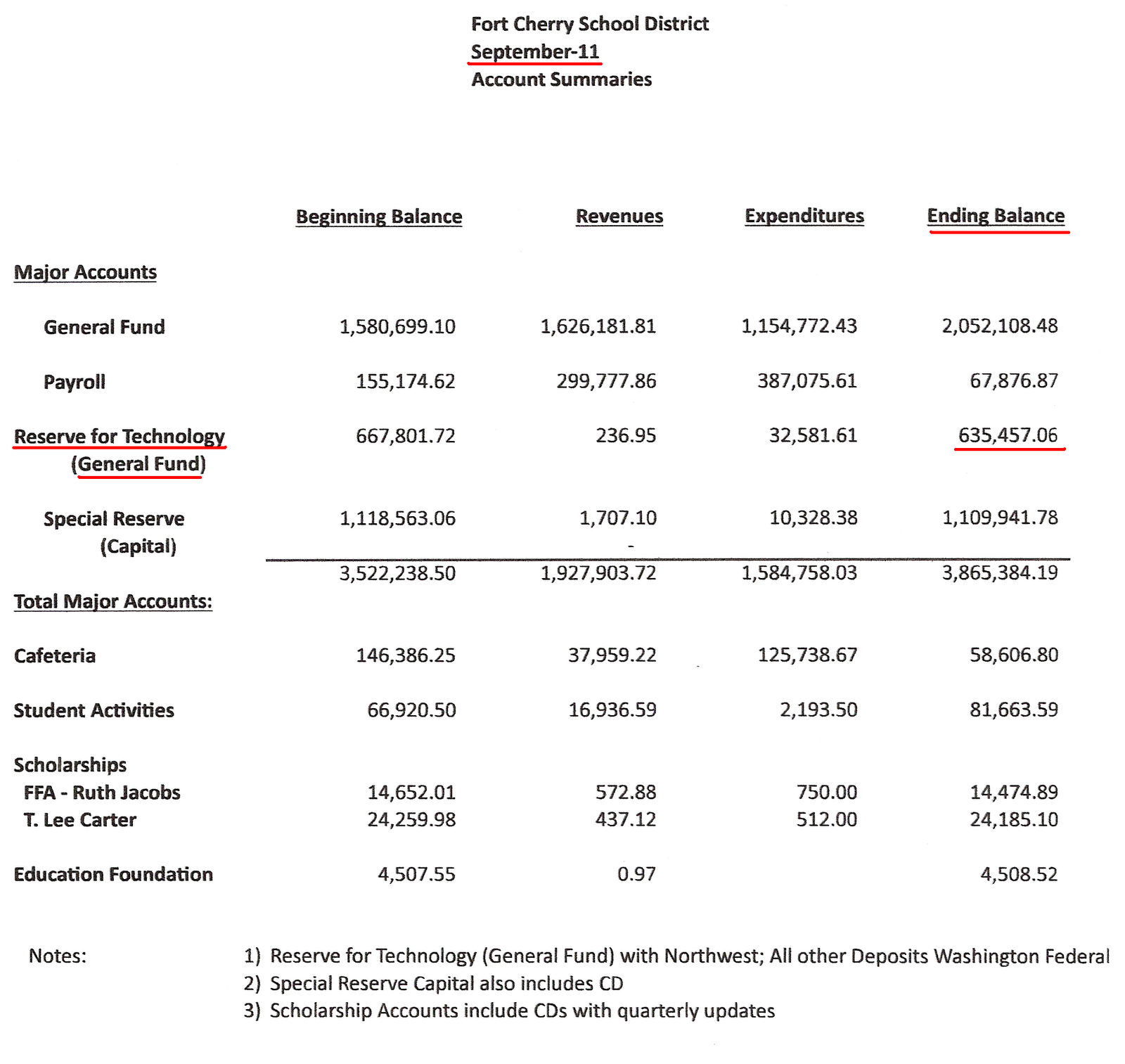

Yet the Committed Fund (and the $1.3 million held in it), does not appear as such on the Account Summaries Sheet that is distributed to the public and given to board members at the monthly board meetings. The Account Summaries Sheet is created each month by Sroka to summarize the balance of FC’s major funds.

The money shown in the Committed Fund on the AFR is actually the money shown as “Reserve for Technology (General Fund)” on the latest Account Summaries Sheet available to the public.

FC reported that fund’s balance as $1,308,589 to the state, but Sroka reported only $635,457, to the public, a difference of $673,132.

Why the $673,132 difference?

Prior to June of 2010, the “Reserve for Technology (General Fund)” was called the “Capital Reserve/Technology” Fund.

As shown in Cypher’s 2007 annual audit, FC’s Capital Reserve/Technology fund was established according to PA school code and as such, was restricted to be used for capital improvements.

Cypher and Cypher

Audit for school year ending June 2007

Although it went against PA School Code, for years FC purchased technology with money from the “Capital Reserve/Technology” Fund.

Possibly to ensure that the state remain unaware that the money was spent on technology instead of capital improvements, this fund was called the “Capital Reserve/Technology” Fund on all internal FC documentation. However, on all state reports it was labeled as “Capital Reserve”.

In addition, FC repeatedly labeled all purchases on state reports as money spent on buildings/improvements, not technology purchases.

Cypher advised FC against spending money from its “Capital Reserve/Technology” Fund on technology. According to PA School Code, Capital Reserve Funds were to be used for capital improvements and the purchase of school buses only, not technology.

Cypher and Cypher

Audit for school year ending June 2009

Effective July 2010, new accounting rules (GASB 54) mandated the reclassification of “Capital Reserve Funds”. Under GASB 54, Capital Reserve Funds were to be reclassified as “Capital Projects” Funds. This newly classified fund would retain the restrictions placed on the old Capital Reserve Fund and also “help financial statement users to better understand the purposes for which governments have chosen to use particular funds for financial reporting.”

Essentially the reclassification makes it blatantly obvious that the money must be spent the way the government intended – for capital improvements - bad news for anyone abusing a Capital Reserve Fund.

At that time, there was dissension between the administration and some board members over the reclassification of that fund. Ultimately, the fund was not reclassified as mandated by GASB 54, instead Dinnen, Sroka, and B. Miller made the following moves:

MOVE 1:

In June of 2010, without board approval, money that was previously held in the Capital Reserve/Technology Fund was reported to the PDE in the 2010-2011 Final Budget as transferred to the General Fund under Budgetary Reserve.

2010-2011 Final General Fund Budget (PDE-2028)

AUN: 101632403 Fort Cherry SD

Printed 8/24/2011 9:46:28 AM v2.0

Even though Dinnen and Sroka called the fund “Special Revenue Fund for Technology” on the document submitted to the PDE, a “Special Revenue Fund for Technology” never existed.

The “Special Revenue Fund for Technology” was actually the “Capital Reserve/Technology Fund” and we believe was purposely mislabeled on this PDE document and others by Dinnen and Sroka – more about this in a future post.

The document, with its misleading information, was signed by Dinnen, Sroka, and B. Miller.

MOVE 2:

Then, in December 2010, in a last minute agenda change, Dinnen, Sroka, and B. Miller slyly maneuvered the board into approving the transfer of all the money ($707,576), out of the Capital Reserve/Technology Fund and into Budgetary Reserve; a move that was reported to the PDE as board-approved six months earlier.

MOVE 3:

Next, in June of 2011, and again without board approval, that money, now up to $710,854, was reported to the PDE on the 2011-2012 Final Budget as a board-approved move into a “Committed Fund”, which Dinnen, Sroka, and B. Miller designated for technology.

0830 Estimated Ending Committed Fund Balance 710,854

“Explanation: This amount is designated for Technology purchases per GASB 54 and School Board approval.”

As in 2010, this 2011 budget was signed by Dinnen, Sroka, and B. Miller.

Why does this matter?

Before the money was moved to a Committed Fund in June 2011, that money was reported to the state by Dinnen, Sroka, and B. Miller as held in Budgetary Reserve.

They earmarked the money for technology; but according to the PA Comptroller’s Office, money held in Budgetary Reserve is simply money held in the General Fund – it’s not designated for any special expenditure or limited for use for any special account.

5900 Budgetary Reserve

Budgetary Reserve is not an expenditure function or account. It is strictly a budgetary account.

PA Department of Education

Manual of Accounting

In other words, Budgetary Reserve can be used for any purpose, such as teacher salaries and programs.

Remember . . . the board, under Dinnen’s direction, voted to eliminate teachers and programs in May of 2011.

Could it be that Dinnen, Sroka, and B. Miller realized that the public would be aware that money in Budgetary Reserve could legally be used for salaries and programs?

So . . .

Just as teachers and programs were eliminated, we see Dinnen, Sroka, and B. Miller make a move to change the status of the money - attempting to get it into a “Committed” Fund and therefore unavailable for things such as paying teacher salaries or maintaining programs.

Money held in a “Committed” Fund is restricted to the use it was committed for – in this case, they designated it for technology.

Back in spring of 2011, with the major cuts in state funding looming, did Dinnen, Sroka, and B. Miller come up with a plan to shield $1.3 million by reporting it to the state as transferred into a Committed Fund?

But . . .

The board never voted to move the money into a Committed Fund as Dinnen, Sroka, and B. Miller claimed on the budget submitted to the PDE.

0830 Estimated Ending Committed Fund Balance 710,854

“Explanation: This amount is designated for Technology purchases per GASB 54 and School Board approval.”

In addition, PA School Code mandates that a board resolution is required to establish a Committed Fund.

0830 Committed Fund Balance

Amounts constrained to be used for a specific purpose as per government’s highest level of decision making authority such as the school board, board of directors, board of trustees, etc. Note: Board Resolution required. Constraint can also be removed or changed by an equal level action.

PA Department of Education

Manual of Accounting

Board resolutions must be submitted to the PDE.

Fort Cherry did not submit a Board Resolution to the PDE because the board never voted to establish a Committed Fund in the first place. No vote, no resolution.

This document confirms that the PDE does not have a resolution from FC.

Therefore, it appears that despite cuts in state funding, FC has had money available all along in the General Fund, enough that it did not need to eliminate teachers and programs.

The school auditor will be at the meeting on Tuesday, January 17.

The public, and the board members we rely on to represent the public, need to ask Mr. Cypher to explain:

· How the money was moved without board approval

· How the money was moved without official board resolution

· Why there is a $673,000 difference in the fund balance

The public, and the board members we rely on to represent the public, need to ask each person - Dinnen, Sroka, and B. Miller - to explain why they signed a document and moved the money without board approval and without informing the public.

The meeting starts at 7:30 p.m.

Please attend.