As explained in the last post, from January 2008 through August 2011, FC administrators and board members have been reimbursed $155,563.33 for expenses and mileage.

Under IRS rules, reimbursements that exceed the amount treated as substantiated are reported on a W-2. Could this be one of the reasons why FC continues to use taxpayer money to fight the release of those documents?

Code L—Substantiated employee business expense reimbursements.

Use this code only if you reimbursed your employee for employee business expenses using a per diem or mileage allowance and the amount that you reimbursed exceeds the amount treated as substantiated under IRS rules. See Employee business expense reimbursements on page 5.

Report in box 12 only the amount treated as substantiated (such as the nontaxable part). Include in boxes 1, 3 (up to the social security wage base), and 5 the part of the reimbursement that is more than the amount treated as substantiated.

Now that we’ve seen one example of the type of expense reimbursement the administrators receive (more will follow), it’s time to take a look at what’s happening with the W-2 appeal.

The facts behind the right-to-know request, Fort Cherry’s denial, and subsequent appeal of the administrators’ W-2s can be found in the 6/27/11 post, http://fortcherryinfo.blogspot.com/2011/06/fort-cherry-school-board-using-taxpayer.html.

Here’s the latest:

As you know from the June 27th post, FC lost the appeal in the Court of Common Pleas.

By FC solicitor (MB&M) recommendation and FC Board approval, Fort Cherry appealed to the next level, Commonwealth Court.

As you continue to read, keep this mind:

· Taxpayer money is paying for the appeal process.

· Taxpayer money is used to pay the salaries, bonuses and expense reimbursements of the administration.

· The public has the RIGHT-TO-KNOW exactly how taxpayer money is spent.

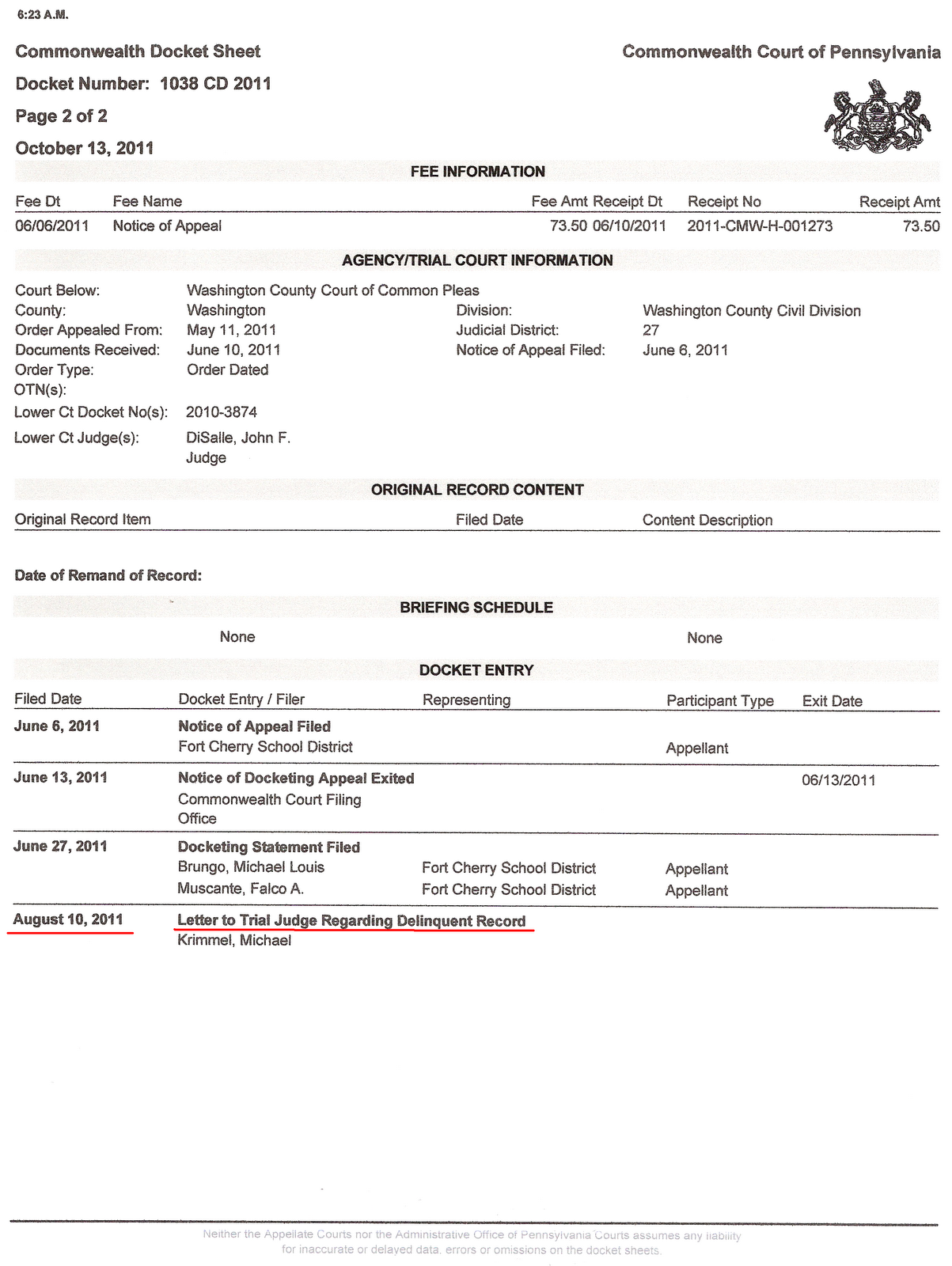

Let’s start with the docket sheet showing the case has moved to Commonwealth Court:

On the last entry on the docket sheet, there is a reference (underlined in red) made to a “delinquent record”.

That entry refers to an Order submitted by Judge DiSalle of the Court of Common Pleas.

In the Order, Judge DiSalle affirms the May 11, 2011, decision by the Court of Common Pleas; a decision which states that the Final Determination from the Office of Open Records should be upheld.

Here is a synopsis of the Order:

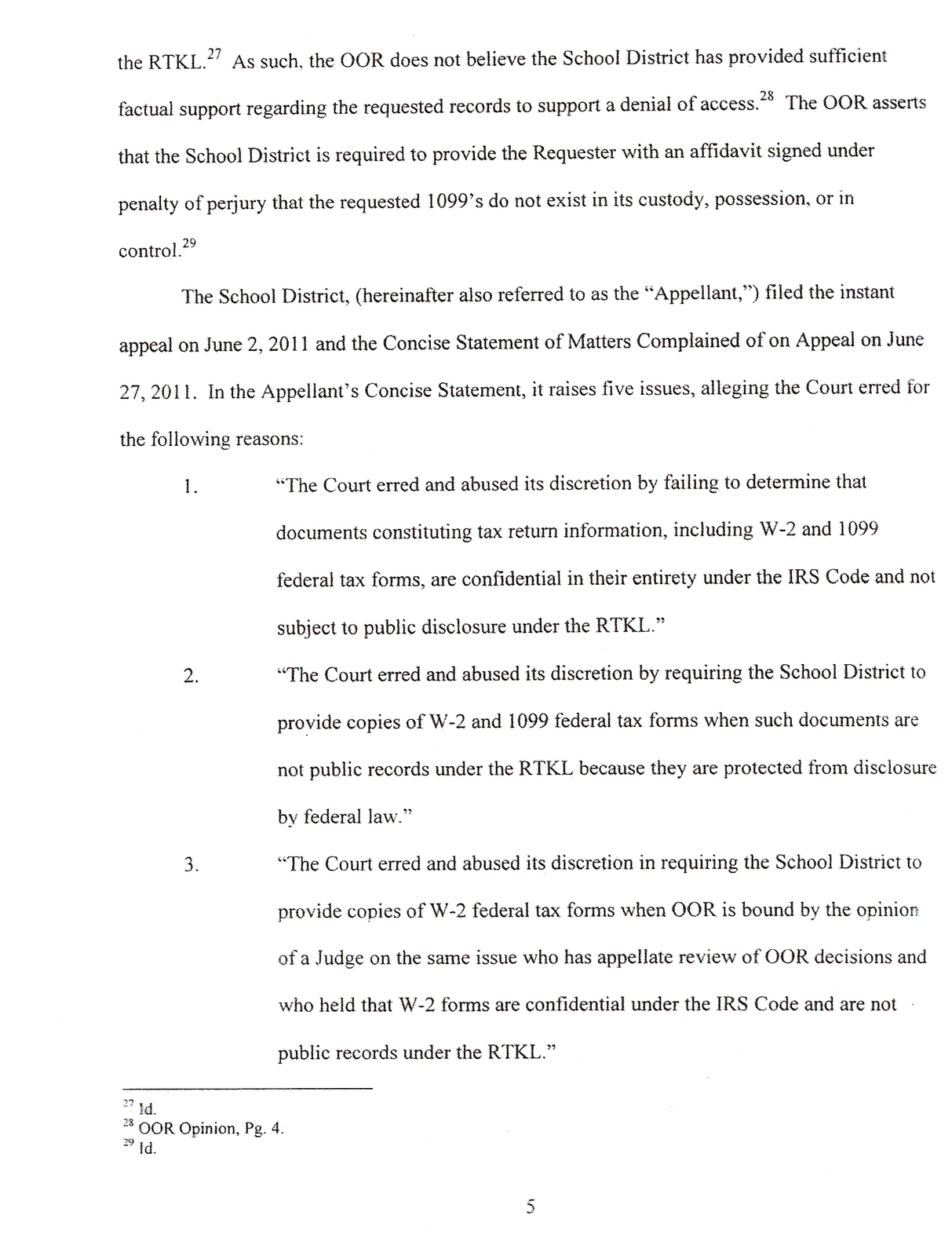

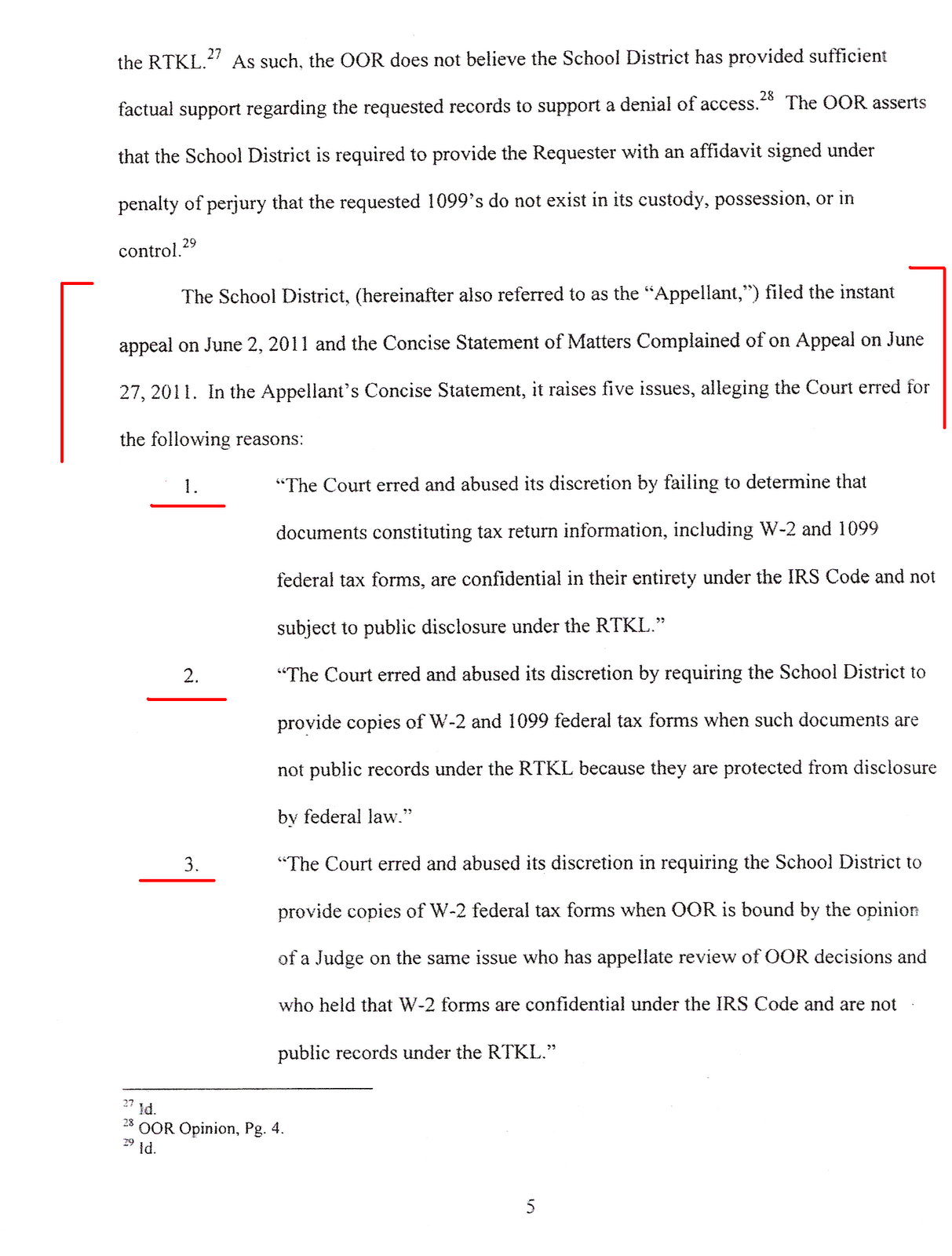

· MB&M/Fort Cherry alleges: The tax forms are confidential under IRS code. The Court erred by requiring FC to provide copies of W-2s and 1099s because they are protected from disclosure by federal law.

· Judge DiSalle upholds: FC did not cite support of this. Instead, FC broadly referenced IRS code.

· MB&M/Fort Cherry alleges: A judge from Monroe County ruled that the W-2s are confidential and the Office of Open Records is bound by that decision.

· Judge DiSalle upholds: A decision from the Court of Common Pleas in one county has no presidential effect on the Court of Common Pleas of other counties.

· MB&M/Fort Cherry alleges: The district does not have to provide the 1099 forms because the appeal was not filed on time.

· Judge DiSalle upholds: The requester filed the appeal on time. This issue has no merit.

· MB&M/Fort Cherry alleges: The Office of Open Records lacks the authority to require FC to provide an affidavit stating that the 1099 forms do not exist.

· Judge DiSalle upholds: To state that a record does not exist without providing a sworn affidavit does not meet the burden of proof. Commonwealth Court has ruled that a sworn affidavit is required to prove the nonexistence of a record and that the Office of Open Records has the authority to require them.

In the Order, partially shown below, Fort Cherry’s allegations and Judge DiSalle’s response are marked in red. A full copy of the Order is shown at the end of this post.

Will the Fort Cherry School Board continue to approve the use of taxpayer money for legal appeals to conceal how the district is spending OUR PUBLIC FUNDS?

A complete copy of the Court Of Common Pleas September 27, 2011, Order is shown below: